WHY THIS MATTERS IN BRIEF

- Bitcoin shows no sign of stopping or slowing down so regulators and governments are now starting to take the regulation and “management” of the “stateless crypto economy” more seriously

A little while ago I gave a talk on the Future of Money, which is undoubtedly crypto, or at the risk of offending the purists among you, digital, sorry, in Amsterdam, and as the world continues to get more accustomed to these relatively new forms of currency it’s clear we’re starting to enter the “What the hell is it and how do we regulate it?” phase of the technology’s cycle.

Recently, when the Chinese government, who, via the People’s Bank of China (PBOC) “quietly” announced they’re going to be one of the first governments in the world to introduce their own national cryptocurrency, announced a ban on Initial Coin Offerings (ICO’s), it looked like they were trying to rein in a rapidly expanding, speculative, “Crypto Economy.” But now, thanks to a leaked document, it looks like it’s the start of a more coordinated campaign to shut down the use of “stateless” cryptocurrency throughout the country.

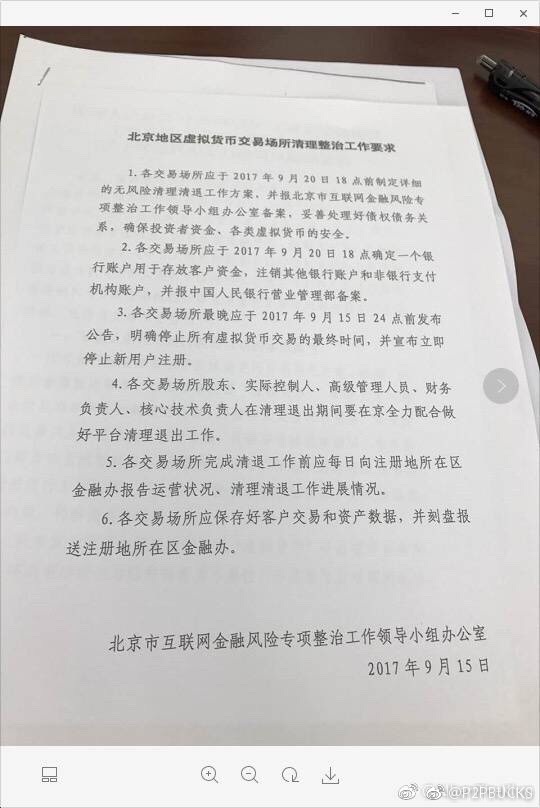

The Letter

Cryptocurrency advocates would call it growing pains with the focus on “pain.”

However, that said it’s likely that there’s a twist in the tail for this story because while the move, the full extent of which isn’t clear yet, that instructs all China’s Bitcoin exchanges to shut down within the month will undoubtedly help “kill” most of Bitcoin’s lofty ambitions in the country it could also give the government the rocket fuel they need to help them establish their own national PBOC cryptocurrency as the bona fide replacement. Chinese users will be given a chance to withdraw their funds before the exchanges shut down.

“BTCChina encourages customers to withdraw their funds as quickly as possible,” one of the exchanges wrote in a tweet, “customers can withdraw their funds whenever they want.”

Bitcoin has always been something of an awkward fit for China which strictly regulates financial markets and limits the flow of funds overseas, and now it seems that Chinese officials have apparently concluded that Bitcoin has become too popular as a way to circumvent those regulations.

Last week Reuters quoted a comment by a senior Chinese official that may help to explain the Chinese government’s thinking on the matter.

Li Lihui, a senior official at the National Internet Finance Association of China and a former president of the Bank of China, told a conference in Shanghai that global regulators should work together to supervise cryptocurrencies.

“Digital tokens like bitcoin, Ethereum that are stateless, do not have sovereign endorsement, a qualified issuing body or a country’s trust, are not legal currencies and should not be spoken of as digital currencies,” he said, “they can become a tool for illegal fund flows and investment deals.”

He also said there should be a distinction between digital currencies, which were being studied and developed by authorities such as the Chinese central bank, and digital tokens such as Bitcoin.

“Digital currencies developed by authorities could be used for good, with the right regulation,” he said.

The Internet finance association was set up by China’s Central Bank, and according to Reuters, it “urged members to abide by Chinese laws and not deal in cryptocurrencies.”

As a consequence, if Li’s comments reflect the thinking of the Chinese authorities, and there’s not much to suggest that it doesn’t or wouldn’t, then that in turn would suggest that this is much more than a temporary halt to Chinese Bitcoin trading, and that, as suspected, the government seems to be laying the groundwork to ban independent digital currencies from the Chinese economy altogether in favour of their own.

If so, that will raise some awkward questions for other Chinese entrepreneurs participating in the blockchain industry. For example, four of the world’s largest Bitcoin mining operations are based in China. Miners process Bitcoin transactions and, in exchange, are rewarded with newly created bitcoin. They also exercise significant power over changes to the Bitcoin protocol, so if Chinese mining pools were shut down, it would have a big impact on the distribution of power in the global Bitcoin economy, and so far, even though only a short time on from the announcement Bitcoin nosedived from its peak of $4,950 to $3,226, although now, it has to be said, it’s recovered some ground and this morning was trading at $3,942 (Courtesy Coindesk chart).

Right now though it doesn’t look very likely that other countries will follow China’s lead, and in the US regulators clearly signalled their acceptance of Bitcoin in 2013, since which there has been little sign that they’d change their stance on the issue.

While a US cryptocurrency ban isn’t likely it seems highly likely that we will see an increase in the amount of regulatory scrutiny of the crypto economy, especially from the Securities and Exchange Commission (SEC), especially in light of the fact that recently there have been a number of cryptocurrency offerings that look suspiciously like illegal stock offerings, something that the SEC has issued several warnings over.

As for China’s latest move though, well, it’ll just go down in history as another weird page in the story of Bitcoin and the crypto economy which in many respects resembles a weed – you can keep stamping on it but it just keeps growing back stronger. As for me I’m off to Starbucks to buy myself a flat white with BTC while I still can.