WHY THIS MATTERS IN BRIEF

- We live in a world full of unprecedented change and opportunity but many business leaders are guided by a historic view of business and industry evolution not a millennial view, the rules of business have changed, this is the time for re-invention not “just” innovation

Over the past year I’ve lost count of the number of times that people at events, or behind closed doors have asked banking executives for their opinions on the future of banking and the threats posed to their businesses and business models by the worlds burgeoning, and vibrant, fintech community, and the answer is almost always the same: “We don’t fear being disrupted by the fintech community, while we of course embrace them, and work with them, if they get large enough, or interesting enough we’ll just buy them.”

When asked about the threat posed by GAFA (Google, Amazon, Facebook and Apple), or more recently FATBAG (Facebook, Apple, Tencent, Baidu, Alibaba and Google) the answer invariably changes: “We’re at risk of turning into a dumb pipe,” harped one senior executive from one of the worlds’ largest banks, “My children don’t even see our bank as a brand,” harps another, and so it goes on. And then the uncomfortable squirming stops and the phrase “but they don’t have a banking license” echoes around the room, and the cold sweats stop. Thank heavens none of them have the right piece of paper…

There is little question in many peoples minds that todays banking elite see technology, such as Artificial Intelligence (AI), Blockchain and “digital” as disruptive to their businesses – or, putting the shoe on the other foot, as an opportunity. After all, not only are these technologies helping to create a new “Internet of Financial Services” but they are also helping to lower the barriers to entry for the thousands of fintechs around the world who want to re-fashion the foundations of today’s modern financial services industry, such as Railsbank who are helping fintechs get “banked” faster. But going head to head with intriguing, often resource limited, fintechs is one thing, going head to head with one of the world’s largest internet giants is quite another.

I recently attended an event where representatives four of the UK’s largest banks stood on stage and extolled their huge mobile user base of 25 million users – a user base that fintechs would die for and a user base that companies like Facebook would just sniff at and roll over on. And I recently presented at one of the world’s largest banks on how their group could be disrupted by a toaster. Yes, that’s right – a toaster (and a fridge).

Disruption comes in all forms.

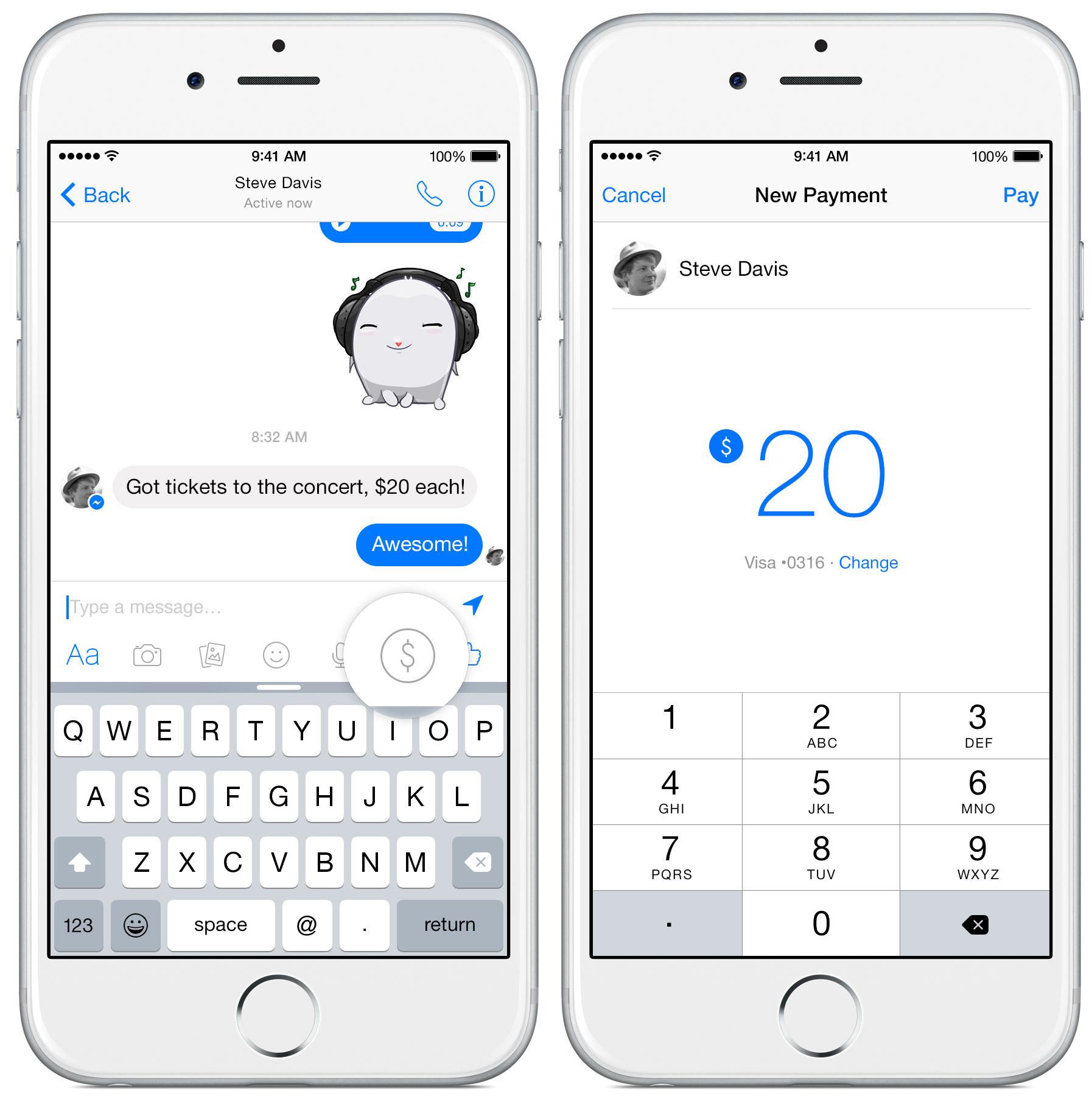

Now, just a month down the line Facebook has finally gone and gotten what most banking executives were fearful of, and while it doesn’t turn Facebook into a bank – there are lots of questions about why they would even want to venture there – their recently awarded E-Money license from the Central Bank of Ireland (CBI), complete with EU passporting rights, which will allow them to extend the service seamlessly to all 27 members of the EU, paves the way for them to roll out friend to friend payments, and more, via their Facebook Messenger app which at last count had over 800 million active users.

The new license, which pertains to “E-Money issuing and payment services provision” will let Facebook Payments International Limited conduct credit transfers, payment transactions and money remittance, and as they start warming up to the idea of offering a range of new financial services products and services via their platform it’s now not just the banks who are courting fintechs – Facebook is allegedly on the prowl as well, and who knows – if they did want to become a bank maybe they’d just buy one…

“In the short term, it means that Facebook Messenger will be able to roll out its peer-to-peer payment features in Europe. It could compete with the likes of Paym or Barclays’ Pingit in the UK, but most likely also democratize peer-to-peer mobile payments which did not take off as quickly as in the US. But there are also open questions about its potential in the mid-term. Is Facebook Messenger going to offer money transfers in all EU currencies, or only in Euro? Will the service be available for cross border transactions within the same currency or extended to cross currency transfers?” says François Briod, founder of money transfer comparison site Monito.

As for Facebook themselves they posted the following statement:

“Facebook Payments International Ltd. (FBPIL) is pleased to confirm we have been approved authorization as an electronic money institution by the CBI. The license enables us to roll out products like charitable donations on Facebook or peer to peer payments via Messenger in Europe. The license authorizes FBPIL to issue donations from Facebook users to charities registered in the European Economic Area (EEA) only; and peer to peer payments, within the EEA.”

While having a piece of paper is one thing what we do know for certain is that Facebook, across all of their properties has a huge user base, full of digital savvy individuals who, it could be argued, are more open to exploring and using these new kinds of services than their parents might have been in the past. We also know that the way people interact with and use technology is changing, for example, the advent of conversational commerce, and that Facebook is a formidable technology savvy organisation that could dominate in a cashless society, and we also know that Mark Zuckerberg recently explored the idea of using Facebook as a Digital ID platform – along similar lines as the ID2020 initiative which aims to give the 2 billion people in the world who have no way of proving who they are – and therefore have no way to secure loans, finance or insurance a portable, electronic ID.

All that then remains is the following, multi billion dollar question: Does Facebook have the desire and will to move into, and offer an “extensive” portfolio of frictionless, digital, financial services?

It certainly has the resources, and there is definitely an underserved segment in the marketplace.

Should today’s financial giants be worried? We certainly know that they “will keep an eye on developments in the space,” as they’d throw out in a press release but in todays hyper networked world where Facebook is at the heart of the new network Facebook could act and deploy much faster than any of todays biggest banks ever could.

Thoughts and answers on a postcard please.

Hey Matthew – nice piece. I’d go further and say that in general, and in this particular scenario; the biggest threat… is the one you didn’t see coming.

Thanks David, I’d agree with you but go one step further, I think that the banks can, or certainly should, be able to see this coming but seeing it coming and acting on it – whether that’s to defend your company against the rise of a new competitor or to grasp it as an opportunity, are two completely different things. Potentially banks may be sitting in the worst camp of all – seeing it coming and doing little to vigorously re-invent themselves or their industry. Tinkering and innovating at the edges are all well and good (and yes they are innovating, they are creating new UI/UX, building digital banks, playing with P2P, prodding blockchain, running accelerators, open innovation communities and sponsoring fintechs etc) but today’s new foes are a different animal. While the banks digitise their back office operations and streamline productivity digitising their businesses simply gets them to the starting line. After all, Facebook and the other millennial tech organisations (GAFA and FATBAG etc) were built on “digital by default,” the hard, painful work – that of re-invention, destruction of the old models and birth of the new models, is yet to happen and that is going to potentially cause them extreme organisational, cultural and financial pain.